Kim-Mai Cutler is quickly developing a reputation as a journalist in technology who provides well-researched commentary on the industry as a whole, particularly around the issues of housing perpetrated by the current tech boom. Her piece on the effect of Facebook on housing prices around that area of the Bay Area is illuminating and shows just how unaffordable that entire area has become.

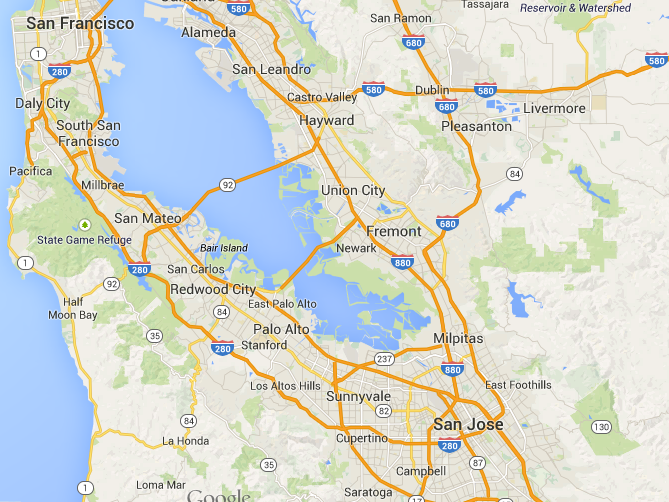

For those not familiar with the geography on the bay, the area is referred to as the SF Peninsula, and it’s a chain of suburban towns sandwiched between two freeways, the US-101 and I-280:

Most of these companies are located from the Palo Alto area down to San Jose. The criticism is that these towns have not really accounted for the population growth as hiring has picked up, and so the market has severely distorted the cost of housing.

There is now no city in that area (which takes ~20 minutes to drive through, so not a small one) where a house can be had for less than $1.1 million[1], and given the data the entire area’s median is probably closer to $2-3 million.

I had written about this trend before, but with actual values it’s easier to reverse engineer how someone would try to buy a house in the area.

- Let’s assume we want a $1.0M, below-median house in Redwood City. You’d have to start by coming up with ~$220k in savings for the down payment + closing costs, and then take out a mortgage for the remaining $800k[2].

- According to Zillow’s mortgage calculator, at 4% interest, this equates to monthly payments of $4,886, with $3,800 going to the mortgage and another $1k towards property taxes (CA property taxes are around 1% per year)[3].

- There’s also maintenance costs to consider, which some have estimated to be as high as 1% of the total cost of the house…per year. I’m going to be cheap and assume a lot of hands on work at around $124/month, so house-related costs round up to a tidy $5k/month.

- A car is pretty much a requirement in the suburbs. Even without accounting for car payments, gas and insurance and tolls will eat up $200-300 per month easily.

- Food, utilities, internet, and living expenses can vary, but this is also the easiest area to cut back if things get tight. I’d estimate this at anywhere from $700 to $1500 a month if we’re being truly thrifty.

So altogether we’re looking at, conservatively, $6k a month to keep a million-dollar home in the valley living paycheck-to-paycheck. We’d of course, have to make a lot more than this in salary:

- The federal taxes will marginally be 25% to 28%, according to the 2014 tax brackets. The effective tax rate should be lower, somewhere around 17-20%.

- Add to that total taxes for medicare and social security, which combine for 7.65%.

- California income taxes should top out at 9.3%, with the effective tax rate also lower, at around 6-8%.

- Even if we’re saving $0 for day-to-day use, I’d at least try to put in some money towards a retirement plan, especially when social security benefits are expected to go down over time. The 401k contribution limit was $17.5k in 2014; I’d try to put $10k in that account a year, or $800/month pre-tax.

Accounting for taxes and some type of retirement savings, the million-dollar home owner will have to make a gross income of:

$6,000 / (100% - (20% + 7% + 8%)) + $800 = $10k/month, or $120k/year.

The good news is that $120k/year is mostly attainable for software engineers in the Bay Area; Glassdoor has the average at around $110k, but I suspect that the data set is incomplete and does not fully reflect the recent boom in engineering salaries[4]. The bad news that for non-developers and non-tech folks, this is an onerous requirement, one that becomes even more unattainable with real monthly expenses: car payments, children, perhaps a small vacation or emergency fund.

Of course, no one would actually be able to get a $800k mortgage with “just” a $120k salary alone; a more realistic debt-to-income ratio would necessitate gross income closer to $140-150k, and probably two income streams (e.g., spouses) at that. Salaries and bonuses and stock grants may be jumping higher in our current boom cycle, but a lot of it is recaptured in real estate.

There’s one huge exception in East Palo Alto, which Kim has also covered extensively. That article is also worth the read. ↩︎

Though honestly, 20% down isn’t that competitive when other offers are in complete cash. ↩︎

To be fair, both the interest and property taxes can be federally deducted when filing taxes, so the true cost is actually around 70% of that amount, fluctuating based on income tax bracket. Getting that money back later doesn’t change how much you have to pay every month, however. ↩︎

Anecdotally, the big companies – Google, Facebook, Apple, etc. – pay substantially more, but not everyone in the area gets to work for a big, cushy tech firm. ↩︎